Debt Recycling Explained: How Australian Homeowners Can Build Wealth More Strategically

Kaine Frew

If you own a home and you’ve been wondering whether there’s a smarter way to build wealth while paying off your mortgage, debt recycling is a strategy worth understanding. With the recent 2026–27 Federal Budget changing the rules around property investment and capital gains tax, the timing to review your mortgage structure couldn’t be better.

For many investors, debt recycling can be a powerful strategy that combines mortgage reduction, tax-effective investing, and long-term portfolio growth.

I’m going to walk you through the basics, what it is, how it works, and whether it might be right for you.

So what actually is debt recycling?

At its core, debt recycling is a strategy that converts your non-deductible home loan into a tax-deductible investment loan. The interest paid on your Principal Place of Residence gives you no tax benefit and is being paid off with after-tax dollars, debt recycling utilises your current debt and turns it into a tax deductible loan.

You don’t take on more debt. You simply replace ‘bad’ debt (your non-deductible home loan) with ‘good’ debt (a tax-deductible investment loan). Over time, your mortgage shrinks, your investment portfolio grows, and the strategy compounds on itself.

For Australian investors and homeowners, debt recycling can be a powerful long-term wealth creation strategy that combines mortgage reduction, tax-effective investing, and investment portfolio growth within a structured financial strategy.

How does it actually work?

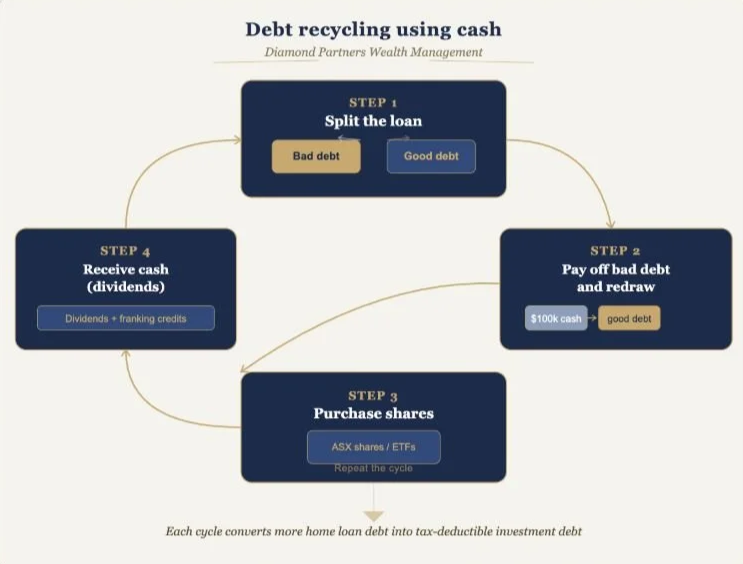

The diagram below illustrates a cycle using the ‘cash method’, one of the most common approaches used in debt recycling strategies for Australian homeowners and investors:

Split the loan: Your home loan is split into two portions. One is your standard ‘bad debt’ (non-deductible), the other becomes your ‘good debt’ (investment/deductible).

Pay off bad debt and redraw: You make a lump sum payment to your non-deductible loan (say $100k), then immediately redraw that $100k as ‘good debt’ to invest. This is the key step. The ATO requires the money to flow directly into investments for the interest to be deductible.

Purchase shares: The redrawn funds are invested into an income-producing portfolio, typically Australian shares or ETFs. This allows investors to begin building a diversified investment portfolio while simultaneously reducing non-deductible mortgage debt.

Receive cash (dividends): The portfolio generates dividends and franking credits. These, combined with your tax savings, are used to make extra repayments on your remaining non-deductible debt — and the cycle repeats.

Each time you repeat the cycle, more of your debt becomes tax deductible, your portfolio grows, and the mortgage shrinks faster than it would otherwise. It builds real momentum over time and can become a highly effective long-term investment strategy when implemented correctly.

What are the key benefits?

When done correctly, debt recycling can deliver three outcomes simultaneously and may form part of a broader wealth strategy for Australian homeowners and investors.

Tax savings: The interest on your investment loan becomes tax deductible. The higher your marginal tax rate, the more you save. Someone on 47% (including Medicare levy) gets nearly half the interest cost back as a tax deduction. This can improve overall tax efficiency and support long-term investment growth.

Faster mortgage repayment: Tax refunds and investment income flow back into your home loan, paying it down quicker than you could otherwise. Over time, this can help reduce non-deductible mortgage debt more strategically and improve cash flow flexibility.

Wealth accumulation: You’re building a share portfolio from day one — not waiting until your mortgage is paid off to start investing. Compounding starts sooner. For long-term investors, this may help accelerate investment portfolio growth and long-term wealth accumulation through the power of compounding returns.

Why is this even more relevant now, post-budget?

The 2026–27 Federal Budget introduced two major changes that directly affect how Australians build wealth through property and approach long-term investment strategies:

The 50% CGT discount has been removed for assets acquired going forward, replaced with cost-base indexation and a minimum 30% tax on capital gains from 1 July 2027.

Negative gearing on established residential property has been restricted for properties purchased after 12 May 2026. Rental losses can no longer be offset against salary or other income.

This makes the traditional established-property investment model significantly less attractive for new buyers and may encourage greater interest in diversified investment portfolios, tax-effective investing, and alternative wealth creation strategies. The deductibility of interest under a debt recycling strategy, however, is based on well-established and unchanged tax law principles — you’re borrowing to invest in income-producing assets, full stop.

For homeowners with equity and a long time horizon, debt recycling through a well-structured portfolio is now one of the more compelling wealth management and mortgage reduction strategies available.

Who is it suited to?

Debt recycling tends to work best for people who:

Own their home with some equity built up

Have a stable, reliable income with surplus cash flow

Are on higher marginal tax rates (37% or 45%)

Have a long investment time horizon — ideally 7+ years

Are comfortable with the ups and downs of investment markets

Are seeking a more tax-effective wealth creation strategy and structured approach to long-term investing

For Australian homeowners and investors, debt recycling is generally most effective when aligned with long-term financial planning goals, disciplined cash flow management, and a diversified investment strategy.

It’s not for everyone. If your income is variable, your loan-to-value ratio is high, or you’re within a few years of retirement, this might not be the right fit. And it must be implemented correctly — the structure of how money flows is critical for the interest to be tax deductible. Getting this wrong can cost you the deduction entirely.

Seeking strategic financial advice before implementing a debt recycling strategy can help ensure the loan structure, investment approach, and tax treatment are appropriately aligned with your broader wealth objectives.

Where to from here?

Debt recycling isn’t a silver bullet, but for the right person in the right situation, it can be one of the most effective long-term wealth creation strategies available to Australian homeowners and investors. It works by making the tax system and your investment returns do part of the heavy lifting on your mortgage — while your investment portfolio builds alongside it.

When implemented correctly, debt recycling can support tax-effective investing, faster mortgage reduction, and long-term portfolio growth within a structured financial strategy.

If you’d like to understand whether this approach could work for your situation, strategic financial advice can help determine whether debt recycling aligns with your broader financial goals, risk profile, and long-term investment objectives.

Disclaimer: This article provides general information only and does not constitute financial or tax advice. Tax outcomes depend on individual circumstances and current legislation. Always seek personalised advice from a qualified professional before implementing any financial strategy.